With a PhD in financial economics, Sean Hundtofte is here to help you understand how macro and micro economic forces affect homeownership — from homebuying to real estate to refinancing and beyond. A former research economist for the Federal Reserve Bank of New York, Sean’s goal is to help you make more informed decisions about homeownership.

If you’re thinking about buying a home for the first time, you may face some uncertainty. Is now a good time to buy? Should you wait? Before this uncertainty scares you off, we want to offer some guidance.

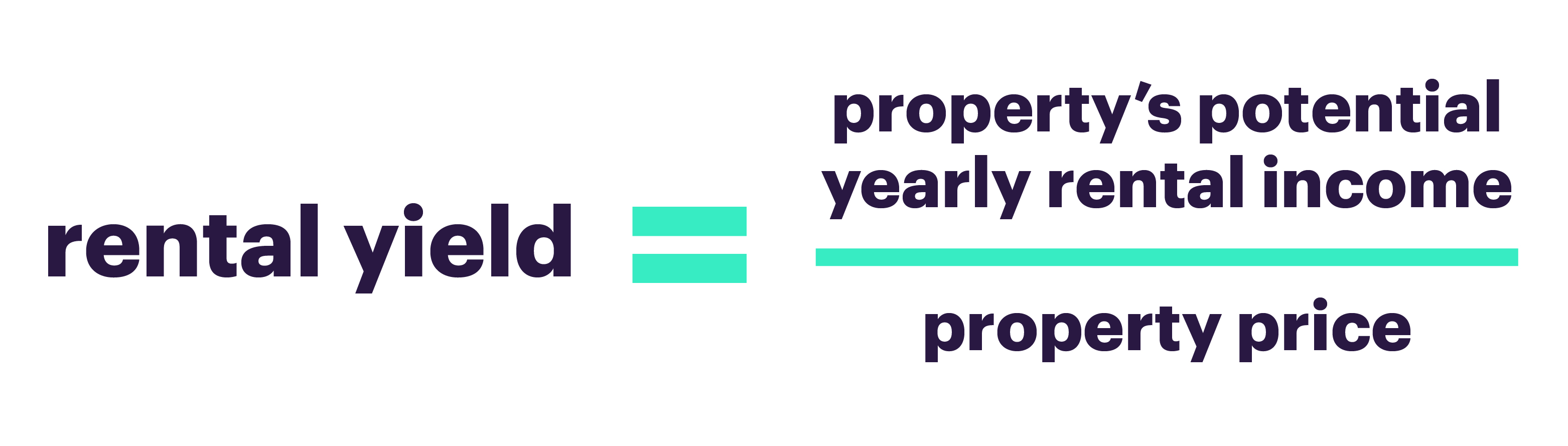

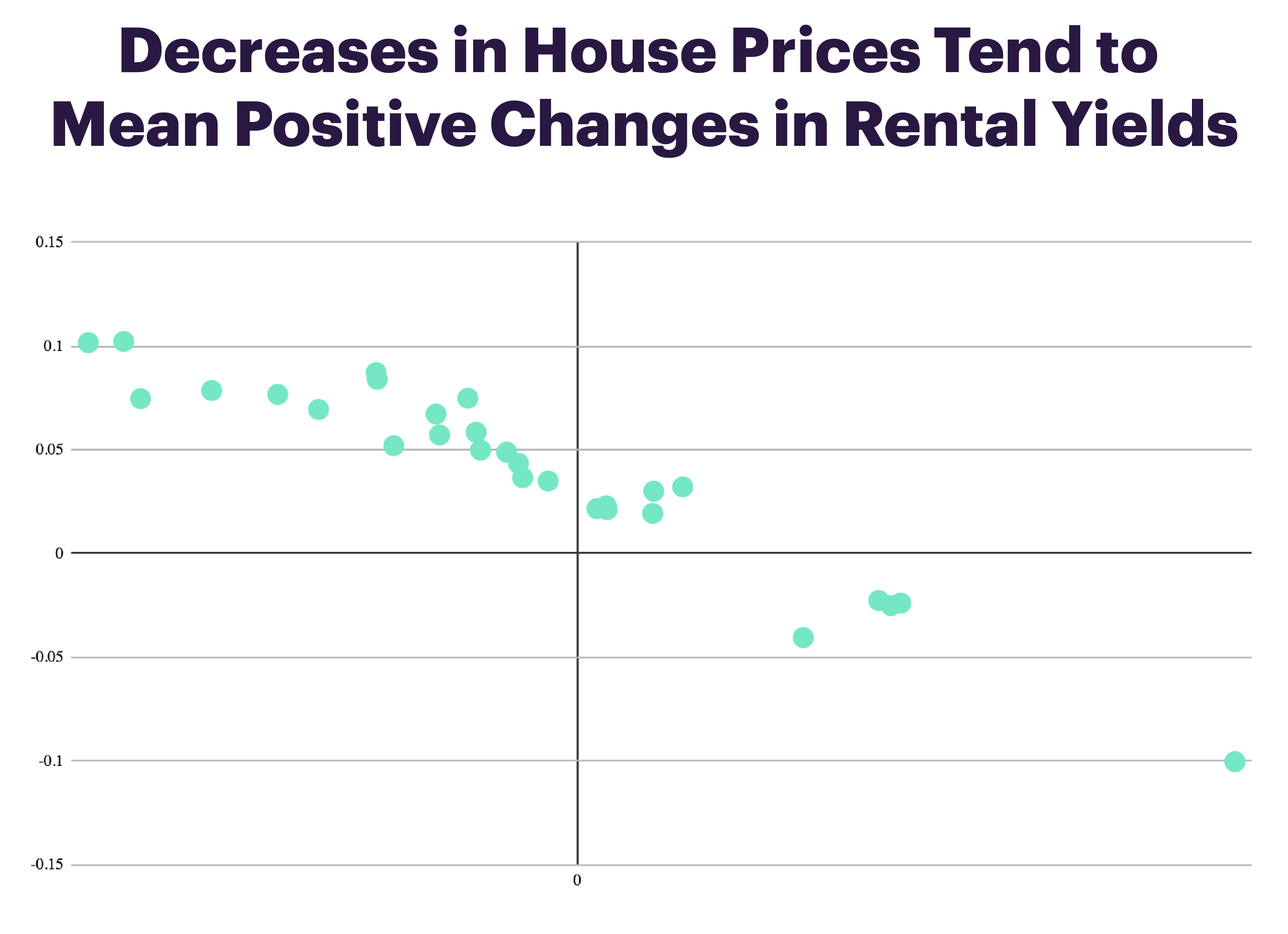

If you started your home search as recently as a year ago, you may have noticed house prices have stalled or decreased in the areas where you were looking.1 If so, what does that mean for you? One way to better understand house prices is to look at the rent-price ratio of a property, also known as its rental yield or cap rate.

Since rents are slow to change, cheaper house prices tend to mean higher rent-price ratios, which is a good thing for you as the buyer. When the rental yield exceeds your potential after-tax mortgage interest rate, it means you can borrow and save money each month by owning a home, compared to renting. You wouldn’t need to wait for further house appreciation to come out ahead, which is a safer position to be in than relying on an increase in house prices to break even.

Source: Davis, Morris A., Lehnert, Andreas, and Robert F. Martin, 2008, "The Rent-Price Ratio for the Aggregate Stock of Owner-Occupied Housing," Review of Income and Wealth, vol. 54 (2), p. 279-284; data located at Land and Property Values in the U.S., Lincoln Institute of Land Policy

In case you haven’t been reading the financial press, interest rates have been going up over the last year. It’s likely because of rosier expectations of growth and inflation, the type of good challenges a healthy economy faces as opposed to the post-crisis challenges we’ve been facing the last decade. Rising rates should lead to higher rental yields if you hold other things constant such as taxes and future house price expectations.

At the same time, however, your cost of borrowing is likely to have gone up over the past year. If you haven’t checked your purchasing power in awhile, now is a good time to check in with us and find out exactly how much house you can afford.

As house prices drop, first-time homebuyers are the clearest beneficiaries because they have no property to sell. If existing owners are looking to upgrade, they might have to sell their current home for less. But as a first-time homebuyer who was perhaps previously priced out of a market or scared away by high prices, now could be a good time for you to buy. Of course you’ll want to take a look at your perfect homebuying scenario and see if something else has happened to deter you from shopping. For example, you might think house prices are likely to drop even further.2 Just remember that prices dropping equals cheaper — and that’s a good thing.

Phew! Are you still with me? So, why all the talk about rent-price ratios and house prices? Even if you don’t plan to rent out your new property, a higher rent-price ratio is a good thing to have. Not only is it a useful way to measure the price of a property, it provides better downside protection (e.g. renting out a room) if you ever lose a job or otherwise face a drop in income.

Overall, a decrease — or increase, for that matter— in house prices shouldn’t solely drive your home purchase decision. We’re simply here to help you interpret macro economic data as you embark on what’s likely your biggest asset purchase. There are many sources for rental information3 and ways to evaluate properties, and we are one source of useful information for you. Have questions? Schedule a call. We’ll help evaluate your homebuying potential as well as the properties you’re considering.

1 In global cities like New York there is evidence that they have fallen while looking at national averages the growth has merely slowed.

2 In the data, there is short-run serial correlation in house price changes (Case and Shiller, 1989) as well as mean-reversion (Capozza, Hendershott, Mack and Mayer, 2002)

3 Craigslist, Zillow, AirBnB...previous rents on the property itself (if available) are great to have.